The Mirage of Private Equity for Retail Investors

Investment firms are making it easier for retail investors to get exposure to private equity . . . but I’m not sure that is a good thing. If you aren’t familiar with the term, “private equity” is just a fancy way to describe investments in private companies not listed on an exchange. Relative to public equities, private equity is far less liquid, far less transparent, and, for investors, far more expensive.

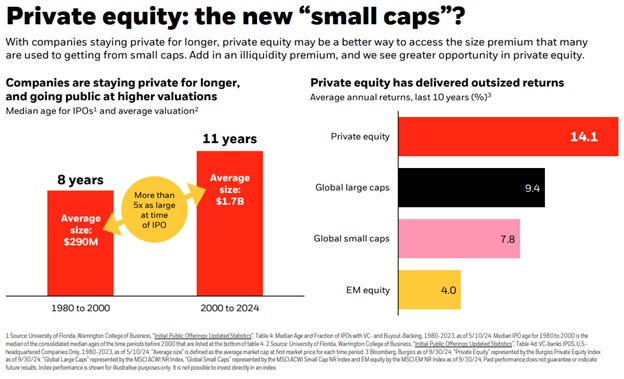

But historically, the returns across the sector have justified the downsides and Ivy League endowments have loved private equity since Yale popularized the allocation in the mid-1980s.

However, things have changed quite a bit over the last few decades, and when it comes to private equity, it is essential to remember that past performance may not be indicative of future returns.

Take this satirical note from Cliff Asness: 2035: An Allocator Looks Back Over the Last 10 Years, in which he imagines what a note to clients will look like ten years from now.

Alas, sadly, and totally unforeseeably, it turned out that levered equities are still equities even if you only occasionally tell your investors their prices (and when you do, you do not really move prices that much). Disappointing, but PE [private equity] acting like equities would have been tolerable if they had actually outperformed public markets, but they underperformed! It seems that eventually, and a 10-year disappointing market counts as “eventually,” even privates have to be (mostly) marked-to-market. We really did not see this underperformance coming. After all, the prior 30 years saw much higher IRRs on private equity than total returns on public equity. What we didn’t count on, I mean who could see this coming, was this outperformance reversing. I mean, what better way is there to estimate what will happen in the future than looking at what happened in the past!?

One super-subtle tipoff we missed was that, like us, every allocator in the world loved privates back then precisely because it didn’t seem that they ever went down a lot—even when the equity market fell sharply. Laundering our volatility made life so much more pleasant and our investments so much easier to live with! Unfortunately, it also turned out that “more pleasant,” especially when everyone is engaged in pursuing the same kind of “more pleasant,” has a cost. So at the end of the day, a lot of managers got paid a **** ton of money for less-than-equity returns, with at-least-as-high-as-equity risk, just so allocators could feel safe in their jobs and to make sure others thought they were on the cutting edge of investing. That was a pretty large payment, like many hundreds of billion dollars over 10 years industry-wide, from our collective investors to our collective managers, just to make our allocator lives easier! A lot of the people who made this allocation decision are not around anymore, so I guess the laundering did kinda work out for some of them.

Even more problematic for retail investors is that private equity funds are starting to offer them allocations simply because the institutional money is trying to find a way out. To quote this article from Institutional Investor:

[Institutional] investors have been hard-pressed to commit more money to private equity, leading to the fundraising shortfall. Bain said that the amount of capital raised in 2023 was the lowest since 2018, down 20 percent from 2022, and almost 30 percent below the record high reached in 2021.

While investors are still bullish on private equity, Bain said that “as a practical matter, increasing allocations will come down to cash flows. LPs have been cash flow negative for four out of the last five years, as unexited assets began to pile up.”

In other words, old investors need to get out, but there are no buyers because interest rates are high, and they haven’t been able to get any of their money back. To get their money back, they need to expand the investor pool . . . which is where these new “opportunities” for retail clients to buyout the institutional come into play.

For a terrific (and prophetic) discussion of private equity, here is a video featuring Warren Buffett and Charlie Munger explaining why they don’t think private equity makes sense for anyone but fund managers.

So before you get too excited about new investment products offering exposure to private markets and reduced volatility, always ask yourself why they need your money? If the answer is they couldn’t get the money from the institutions, you should probably consider going in another direction.

Personal note:

Claire is a volunteer at Jenni’s Rescue Ranch. She’ll bathe, bottle feed, and generally entertain the puppies.

If you are in the market for a new dog, she highly recommends you check them out.

Thanks / always good

When it comes to writing about investments, the disclaimers are important. Past performance is not indicative of future returns, my opinions are not necessarily those of TSA Wealth Management and this is not intended to be personalized legal, accounting, or tax advice etc.

For additional disclaimers associated with TSA Wealth Management please visit https://tsawm.com/disclosure or find TSA Wealth Management's Form CRS at https://adviserinfo.sec.gov/firm/summary/323123